This post originally appeared at https://www.badgerinstitute.org/2023-wisconsin-income-tax-rate-reform-vetoed/

Why lost opportunity to cut taxes is devastating for the Badger State

The mainstream media, with no historical memory, will invariably focus on what Gov. Tony Evers did today to the most recent Republican plan to cut taxes.

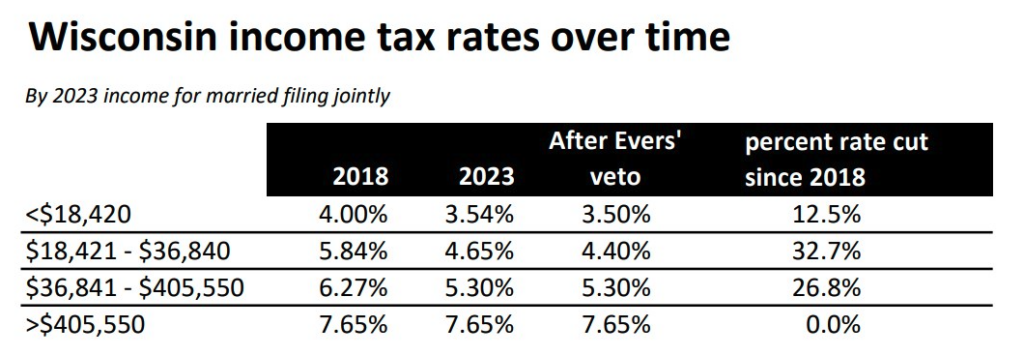

Here’s that story: in sum, he killed virtually all Republican tax cuts except for the two lowest brackets. Those apply only to taxable income under $36,840 per year for married couples. Evers passed up a golden opportunity to give anyone at all making over $36,840 any sort of break on the next dollar they earn, even though Wisconsin has accumulated an enormous multibillion-dollar surplus.

| 2022 Rates for Married Payers | Republican Plan Vetoed by Gov. Evers | Gov. Evers Tax Rates Going Forward |

| Income up to $17,010 paid 3.54% | Income up to $18,420 would have paid 3.5% | Income up to $18,420 will pay 3.5% |

| $17,011 to $34,030 paid 4.65% | $18,421 to $36,840 would have paid 4.4% | $18,421 to $36,840 will pay 4.4% |

| $34,031 to $374,600 paid 5.3% | $36,841 to $405,550 would have paid 4.4% | $36,841 to $405,550 will still pay 5.3% |

| Over $374,600 paid 7.65% | Over $405,550 would have paid 6.5% | Over $405,550 will still pay 7.65% |

There are multiple points of necessary context here:

The cuts that did survive are not significant

There are over 3.2 million tax returns filed each year in Wisconsin. About 677,000 of those, according to 2021 data, pay no income taxes at all for a variety of reasons: the sliding scale standard deduction, the refundable earned income tax credit, business losses, etc. In 2021, only 762,000 returns fell in the two lowest brackets (at the time either 3.54% or 4.65%). So the state will go on penalizing upward mobility for at least three out of four taxpayers because of the changes that became law Wednesday.

And those in the lower two brackets won’t save much because they don’t pay much. Taxpayers (all filers, regardless of type of household) in the lowest tax bracket in 2021, for instance, paid an average of $162 in state income taxes. Those in the second-lowest bracket paid an average of $581.

Gov. Evers did nothing to relieve the marginal tax rate for approximately 76% of all Wisconsin taxpayers

This includes everyone in the middle class who (filing as a married couple) makes over $36,840 per year.

Perhaps the most astonishing thing the governor did, purely from a political standpoint, was his veto of the Republican plan to cut the second highest rate — which applies to the next dollar earned by everyone who makes between $36,840 and $405,550 — from 5.3% to 4.4%.

It’s hard to fathom why he gave Republicans the ability to point out that he failed to so help families earning as little as $37,000 a year at a time there is plenty of money available. Perhaps it was because he didn’t want his progressive base to attack him for also giving a tax cut to those in the same bracket who make up to $405,550 — or even to filers making half of that.

In fact, his veto message criticized Republicans for proposing a plan wherein roughly half of the tax cuts “would go to filers with incomes above $200,000. Under this proposal, 11 taxpayers who make over $75 million per year would receive an average cut of $1.8 million per year.”

It is troubling that in a state where there are more than 3 million taxpayers, he focuses on 11 of them – and ones we need to stick around.

The longer Gov. Evers is in office, the more progressive our tax code becomes

The trend that is antithetical to what is going on in the rest of America.

The lower rates in Wisconsin have been reduced repeatedly in recent years while the top rate has stayed the same — exactly the opposite of what is needed to spur growth and opportunity.

One of the problems with vilifying those high earners is that they really do pay a lot in taxes

In 2021, filers who made over $200,000 earned 29% of all income in this state and paid 36% of all taxes. If we stick just to those in the top bracket, such taxpayers earn about 24% of all income and pay about 32% of all income taxes. If they leave — and some will — the rest of us will have to pay the share they currently cover. Retaining high earners, then, is just one of the reasons it would have been a very good idea to cut both of the top rates.

Badger Institute research for years has pointed to the necessity for reform of Wisconsin’s highly disproportionate, or “progressive,” tax system.

Not only is Wisconsin’s top rate among the highest of state rates, it’s higher than any neighboring state but for Minnesota, and higher than the top rate of any state between New York and California, the Tax Foundation’s Katherine Loughead found in a major 2022 paper laying out options for tax reform.

Worse, Wisconsin’s highest marginal rate, unchanged even as the lower three brackets have been cut over recent years, especially hits Wisconsin employers. About 95% of Wisconsin businesses are “pass-through” entities, meaning their business income is “passed through” to their owners’ personal tax returns. About 67% of such businesses’ earnings are subject to Wisconsin’s highest tax rate, according to Loughead.

As a result, Wisconsin’s tax code incents business owners to move or grow their operations in other states with low or no income taxes.

That isn’t speculation. Nationally prominent economist Don Bruce of the University of Tennessee quantified the benefits that tax reform would have on Wisconsin. In a paper for the Badger Institute this spring, Bruce found that moving to a proportionate, or flat, system levying a 5.1% rate would generate nearly $7.2 billion in additional GDP, $614 million in new investment, and nearly 24,000 additional jobs over the next five years.

Bruce was modeling one of the proposals in the Badger Institute / Tax Foundation paper — one that took advantage of Wisconsin’s sliding-scale standard deduction to ensure that no taxpayer, not even those now paying a lower marginal rate, would see an increase in taxes. Not only would every taxpayer see a lower tax bill as reform returned the persistent surpluses the state now is taking over and above its needs, every Wisconsinite would benefit from the increased business activity tax reform would bring about. As Bruce put it:

“A shift to a flat-rate individual income tax in Wisconsin would represent meaningful tax reduction for many Wisconsin businesses, which then should result in lower price growth, higher wage growth, more employment and higher shareholder value.”

You can read all of the Badger Institute’s research and writing on tax reform here.

Mike Nichols is the President of the Badger Institute and Patrick McIlheran its Director of Policy. Permission to reprint is granted as long as the author and Badger Institute are properly cited.

The post Evers vetoes historic reforms to Wisconsin income tax rates appeared first on Badger Institute.